We are going to do two calculations with a timescale of 30 years. You can do them for a shorter timescales but I don’t see the point because it is the compounding effect over long time that makes this whole exercise interesting.

Imagine you are currently 30 year old and plan to retire by 60. You have steady salary and you want to build your own house. Housewarming is always a good story to tell to your peers. Should you build it now or should you put money into a “house fund” and build the house when you retire and live in a rented house? I’ll suggest that the later (delayed gratification) is at least twice as cheaper than the former (instant gratification) over the timescale of 30 years.

To simplify calculations, let’s assume that you are planning a 1Cr (₹10 million) house. If you take a home loan repayable over 30 years, your EMI will be ₹77,601 per month at 8.60% interest. This is the cost per month of the base case of building house here and now.

Return by pension fund after 30 years when Rs. 57,601 per month is deposited every month.

Second option is that you rent the house and invest the rest of the money into a fund so that after 30 years, you can build the same house. I think you can rent such a house for ₹15,000 to 20,000 in my neighborhood. I am going to use 20,000 per month rent and I am going to assume 5% increase on the rent per year. You will spend Rs. 66 lacs on rent over 30 years.

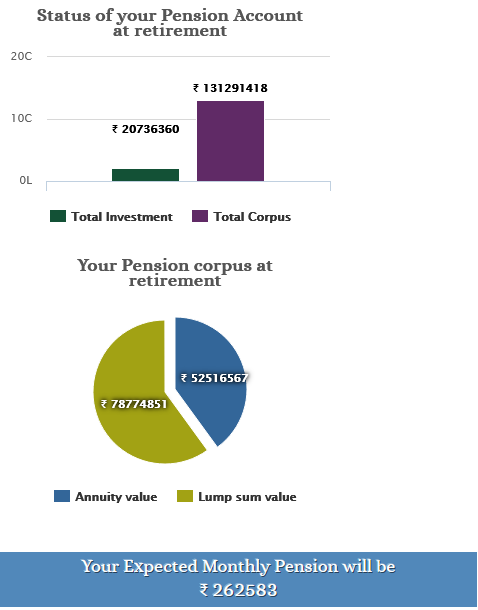

I still save ₹57,601 per month (77,601 EMI – 20,000 rent). If I put all of this into the national pension scheme (NPS) for 30 years, and with a moderate 6% return, you will get ₹7.87 Cr as lumpsum and ₹2.62 lacs per month as pension!

If you have this amount of money in your savings, you can probably build the house and avoid the pain of EMI. However, according to the math, it is still a bad idea.

The question you should be asking — at least for this exercise — is your 1Cr house today available for 7.87 Cr after 30 years? It will be much cheaper unless your house continuously appreciating over 7% per year for over 30 years!

| 1 Cr house today after 30 years | |

|---|---|

| Assuming 3% YoY appreciation | 2.42 Cr |

| Assuming 5% YoY appreciation | 4.32 Cr. |

| Assuming 10% YoY appreciation | 17.00 Cr. |

Assuming a 5% appreciation on your house (only land appreciates, the house depreciates), your 1 Cr house will be worth 4.32 Cr after 30 years. The EMI is at least twice as costly and we are ignoring the monthly pension that comes with pension scheme. In an Index fund, assuming no inflation, an investment of ₹13,000 per month will give you a return of 4.6 Cr. So effectively, making a house after 30 years while living on rent will cost you ₹33,000 per month compared to ₹77,601 per month if you build your house using loans.

I have not considered inflation into any calculation. While inflation is a complicated subject, we can safely assume that your salary will have some protection against inflation. So you can increase the investment to compensate for the inflation. I am not sure if the land price and rent appreciation available on some sources that I have used are already adjusted for inflation?

I don’t think building house on loan is a rational choice.